Big Changes Are Coming to the Payments Industry: Here’s What You Need to Know

Since Visa’s new Acquirer Monitoring Program (VAMP) went live in April 2025, the effects have been immediate—and, for some merchants, severe. Many businesses have already seen their merchant accounts frozen or terminated by payment providers like Shopify Payments and other acquirers due to non-compliance with Visa’s new risk rules.

These closures highlight just how aggressively acquirers are now enforcing Visa’s fraud and dispute thresholds under VAMP.

The transition has not been smooth for everyone. Merchants who ignored early compliance guidance or failed to adjust their dispute ratios have found themselves suddenly unable to process payments — an unprecedented wave of enforcement across the high-risk sector.

What Is VAMP?

VAMP is Visa’s way of modernizing how it monitors fraud and disputes. It aligns with the company’s effort to drive down fraud, chargebacks and enumeration attacks in the card-not-present environment. Fraud and chargebacks are challenges that arise when customers dispute a charge or when fraudulent transactions occur. These issues cost money, impact customer trust, and can lead to penalties from Visa.

In the past, Visa tracked these problems in two separate programs:

- VDMP: Focused on chargebacks (when a customer disputes a charge).

- VFMP: Focused on fraud notifications (alerts from banks about suspicious transactions).

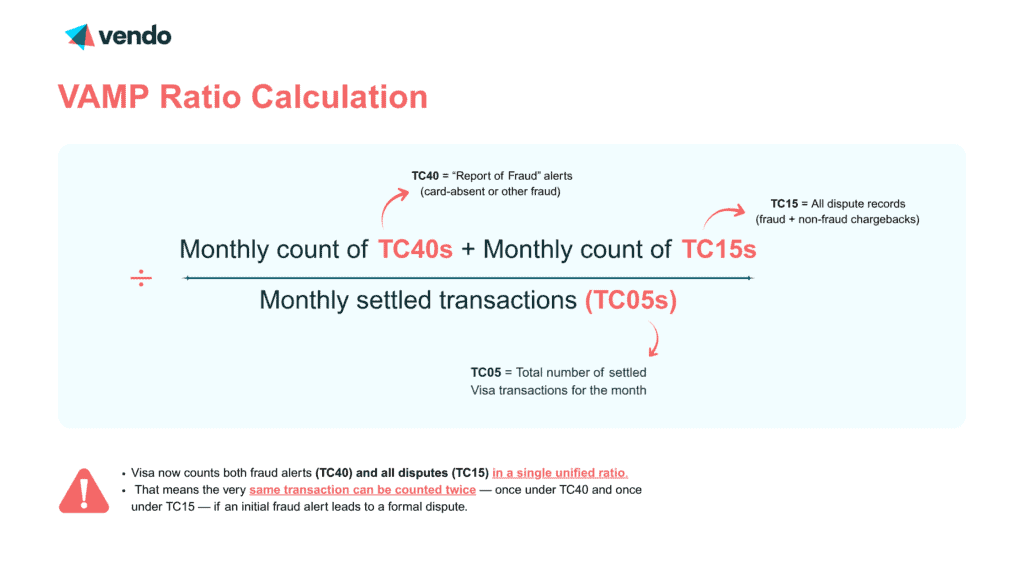

❗Under VAMP, these two programs are merged, and Visa introduces a single “VAMP Ratio,” calculated as the count of both fraud alerts (TC40) and disputes (TC15) divided by total settled card-not-present transactions (TC05).

Key VAMP Details

What Counts Toward the VAMP Ratio?

- Fraud alerts: Known as TC40 notifications, reported by card issuers.

- Disputes: Counted via TC15 records (both fraud and non-fraud) unless the dispute is resolved early via accepted pre-dispute tools and the data extract timing qualifies.

Thresholds & Enforcement Timeline:

- Effective June 1, 2025, updated thresholds and minimum event counts apply across Visa’s programs.

- From April 1, 2025 to September 30, 2025, VAMP was in an advisory phase (no penalties).

- Starting October 1, 2025, full enforcement begins merchants and acquirers may face fees, monitoring or restrictions if their ratios exceed thresholds.

- The publicly published acquirer-level thresholds (for example: Excessive for acquirers at ≥70 bps) are explicitly stated in Visa’s fact sheet.

- Merchant-level thresholds vary by region and are less clearly published by Visa. Many industry sources refer to values like ~2.2% currently, tightening to ~1.5% in 2026.

If your VAMP Ratio exceeds the applicable thresholds, Visa may apply program fees, monitoring requirements, or additional restrictions.

How VAMP Affects High-Risk Merchants

High-risk industries are more likely to face fraud and disputes because of the nature of their business. For example, adult platforms may deal with unauthorized card use; CBD merchants often face regulatory ambiguity and higher dispute rates.

❗Under VAMP, acquirers are now more accountable — their portfolio performance (which includes your merchant activity) is monitored. So even if your own MID looks fine, your acquirer’s overall performance may drag you into increased risk.

With VAMP, it’s essential for merchants to actively reduce fraud and manage chargebacks to stay compliant and avoid penalties.

Steps to Prepare for VAMP

Here’s how merchants can get ready:

1. Understand Your Current VAMP Ratio

- Contact your payment provider to get your fraud and chargeback data.

- Calculate your ratio: Add the number of TC40 fraud notifications and chargebacks, then divide by your total transactions.

2. Improve Business Practices

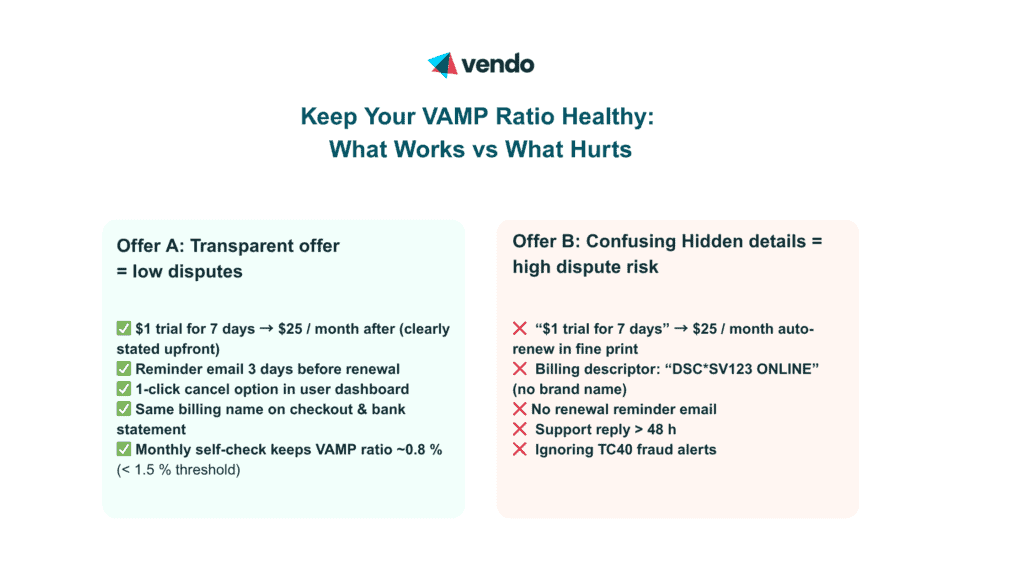

- Avoid low-value transactions: For example, a weekly subscription at $7.50 may lead to more disputes. Switching to a monthly plan at $30 reduces these risks.

- Be transparent with customers:

- Use clear checkout pages that explain pricing.

- Send reminders before charging recurring payments to reduce surprise disputes.

3. Use Dispute Resolution Programs

- Rapid Dispute Resolution (RDR): Automatically resolves disputes by issuing refunds before they escalate to chargebacks.

- Cardholder Dispute Resolution Network (CDRN): Provides a way to resolve disputes directly with customers.

Both tools help reduce chargeback rates by addressing disputes through RDR and CDRN before they escalate further.

4. Strengthen Fraud Prevention

- Use advanced fraud detection tools that fit your industry.

- Regularly review fraud trends and update your systems to block suspicious activity.

Real-World Examples

Example 1: Gaming Merchant

A gaming company struggled with a high VAMP Ratio due to frequent weekly micro-billing and unclear subscription terms. This caused an increase in customer confusion and “friendly fraud” disputes, pushing their combined fraud and dispute rate above Visa’s acceptable range. To fix this, the company:

- Shifted from weekly to monthly billing, reducing transaction frequency and total dispute volume.

- Revised their checkout and email receipts to include clearer refund and cancellation policies.

- Enabled 3-D Secure (2.2) on all high-risk transactions and implemented AI-based device fingerprinting to block repeat offenders.

Within three months, the merchant’s VAMP Ratio dropped from 1.8% to 1.2%.

Example 2: An Adult Entertainment Platform

This platform dealt with many fraud alerts. The merchant took action by:

- Implemented real-time velocity filters, automatically blocking card-testing attempts.

- Integrating Rapid Dispute Resolution (RDR) and CDRN, resolving small-value disputes automatically before they counted toward their VAMP totals.

- Deploying Compelling Evidence 3.0 (CE 3.0) to successfully fight fraudulent chargebacks with geolocation and session-based proof.

After six months, fraud notifications dropped by 70%.

How Vendo Supports Merchants

At Vendo, we make compliance with VAMP straightforward. Here’s how we help:

- Automatic Enrollment: All Vendo clients are enrolled in RDR and CDRN programs to reduce disputes.

- Chargeback Management: We handle chargebacks using advanced tools like Compelling Evidence 3.0 (CE3.0) to recover revenue efficiently.

- Transparent Reporting: Our tools give you a clear view of your VAMP Ratio so you can monitor your progress.

- Expert Guidance: Our team helps you implement best practices to stay compliant and avoid penalties.

Why VAMP Is an Opportunity

While VAMP introduces stricter rules, it also helps merchants build stronger businesses:

- Reduce fraud and disputes.

- Gain customer trust through better practices.

- Stay competitive in Visa’s ecosystem.

Let’s Get Started

Have questions? Want to learn how Vendo can guide your business through these changes? Contact us today to ensure you’re ready for VAMP.

Vendo specializes in high-risk payment processing for CBD, seeds, and other high-risk industries. Our solutions are tailored to meet the unique needs of your business, ensuring seamless transactions and reducing the risk of payment disruptions. Contact our expert team to learn how we can help your business to maximize growth during the festive holidays and beyond.