When merchants fully understand the moving parts of credit card processing and their interaction, it can help to demystify the process and support the handling of potential roadblocks as they arise.

When a person makes a purchase with a credit card, it takes seconds to process. But, there’s a lot going on behind the scenes that the average consumer—or even a merchant—may not realize. When merchants fully understand the moving parts of credit card processing and their interaction, it can help to demystify the process and support the handling of potential roadblocks as they arise.

This allows merchants to do everything within their power to ensure a smooth credit card processing experience—and thus maximizing their revenue potential.

Identifying the Primary Players in Credit Card Processing

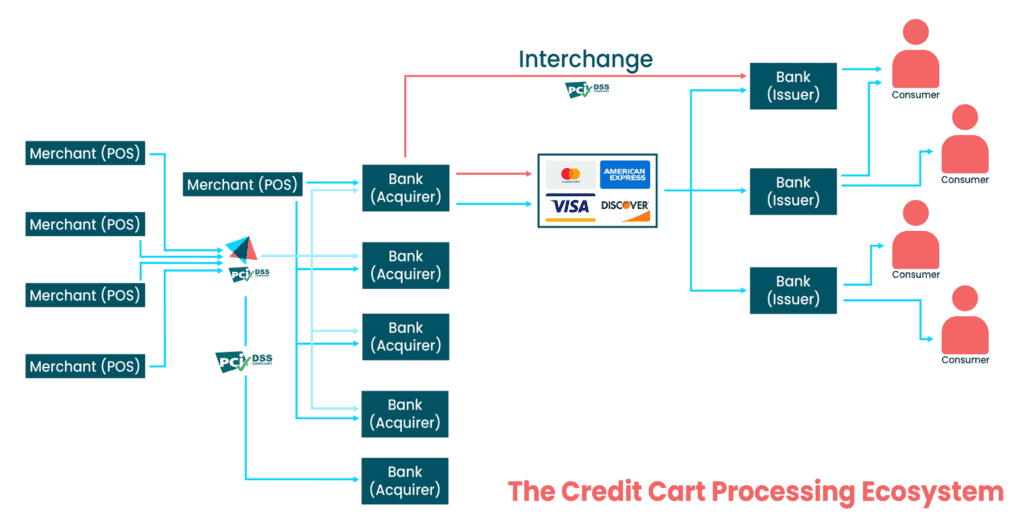

In credit card processing, there are five key players:

- Merchants

- Acquiring Banks

- Credit Card Companies (VISA/Mastercard/Discover/American Express)

- Issuing Banks

- End Users/Consumers

- Payment Facilitator/Payment Processor

When a merchant sets up an account to process payments online, they receive a code from the acquiring bank to include on their website—one which allows the merchant to then accept and process card payments. The acquiring bank has agreements with VISA, Mastercard, etc., who act as the “go between” entity between the acquiring bank and the issuing bank.

The issuing bank is the bank that provides credit cards to end users/consumers. For example, let’s say a consumer opens a bank account with Wells Fargo or Barclays; that issuing bank would give the consumer a credit and/or debit card.

When a consumer makes an online purchase, the acquiring bank communicates on behalf of the merchant through the VISA/Mastercard network, to the issuing bank, to relay the purchase amount. For example, if the purchase price is $75, the issuing bank needs to verify that the consumer has sufficient funds in their account to pay that amount.

At this point, if a debit card is used, those funds are released immediately. With a credit card payment, the issuing bank authorizes (also known as “blocking”) the funds. They’re not yet taking the funds. The funds are only released (or “captured” in industry terms) when the product or service is delivered.

In some cases, authorization (blocking of funds) and capturing of funds occur simultaneously. For instance, with subscription services like Netflix or Spotify consumers are granted immediate access to the service. But, if a person buys a product on Amazon for example, capture of funds doesn’t occur until the product has been delivered (or at least sent via the courier).

In most cases, it’s a seamless process. Yet, there are circumstances in which the communication, authorization, capturing, and more can go wrong. That’s when enlisting a third party payment processor can be highly beneficial.

Top Benefits of Using a Payment Processor

Third party service providers, like Vendo Services, assist merchants in their credit card processing efforts. There are multiple reasons why a merchant might be interested in a third party provider.

Experience with merchant accounts. Merchants, especially smaller merchants, may not have the financial resources, expertise, or banking relationships necessary to establish and maintain their merchant account. Setting up such accounts includes integrating the necessary coding information into the merchant website or app. Even if the merchant hires someone to do just that part, there’s still the matter of maintaining the merchant account. Plus, banks may not want to work with smaller merchants. A third party provider can do all the heavy lifting and present the merchant to the acquiring bank–one that the payment processor may already have a pre-existing relationship with.

Risk of an acquiring bank “going down”. Technology doesn’t always work the way we need it to. If a merchant is large enough to work with multiple acquiring banks, losing access to one temporarily due to a tech issue may not be that big of a deal. But, for smaller merchants, the acquiring bank’s downtime could mean hundreds or thousands in lost revenue. Payment processors like Vendo can help because they maintain relationships with multiple acquiring banks, and therefore, are able to support merchants of all sizes.

Managing global transactions. When acquiring banks and issuing banks are in the same region, the acceptance ratio is much higher. So, if an acquiring bank and issuing bank are both in the United States, transactions tend to encounter fewer declines. On the other hand, if the acquiring bank is in the U.S. and the issuing bank is in Spain (for example), that might raise red flags. A third party vendor who supports merchants worldwide can help because they understand the benefit of geographic proximity, bin mapping, and maintaining banking relationships in multiple regions.

Navigating necessary licenses. Some types of transactions require certain certification. For instance, with subscriptions, merchants need to be able to store credit card information. This requires PCI compliance, which involves a set of security standards designed to ensure that all companies that accept, process, store or transmit credit card information maintain a secure environment. It is mandated by the credit card companies and requires a yearly audit—a tremendous expense, especially for smaller merchants. Third party vendors mitigate those costs due to their expertise in complying with PCI standards and experience in handling related audits.

Assisting high-risk merchants with special challenges. High-risk merchants have especially challenging obstacles when it comes to payments processing. Compliance is a big one; for example, high risk merchants must verify that they are not engaged in nefarious activities. While not insurmountable on one’s own, merchants can expedite getting their merchant account approved and set up when relying on a third party vendor that can help navigate the compliance requirements specific to the high-risk industry.

Identifying fraud and other risks in a timely manner. Payments processors are not just processing the transactions of one merchant, but for hundreds or thousands of merchants. This means they are able to pick up on fraudulent activity—such as stolen credit card numbers at the hands of hackers—much faster than an individual merchant could do on their own. At that point, the processor can block the issuer and prevent any further fraud from occurring. At Vendo, we use a sophisticated fraud identification system powered by Artificial Intelligence (AI) that not only monitors millions of transactions, but also learns from them to help merchants stay ahead of the latest fraud techniques.

Perhaps most important is that a third party vendor like Vendo has both the technological bandwidth and the customer support expertise to ensure merchants avoid the potential pitfalls of credit card processing. One example is if a server experiences a disruption, we can immediately switch to or open up new servers. In most such cases, the merchant may not even know of the problem because of our ability to intervene in real-time.

From a merchant support perspective, we are able to troubleshoot issues (e.g. chargebacks, declines) on behalf of merchants in a way they would never be able to on their own. There are millions and millions of data pieces transacting at one time, and at any given moment a step in the process can go wrong. A third party vendor has the access and the ability to mitigate these issues. Vendo further supports merchants with an expert team who can help prevent such problems and provide pathways to avoid interruptions.

The Bottom Line

If you’ve made it to the end of this blog, you might start to feel overwhelmed as a merchant in your ability to securely, efficiently, and effectively process credit card transactions! At Vendo, we believe that should never be the case. By partnering with a competent and innovative payments processor who not only understands the ecosystem of credit card processing—but actually excels at it—you can focus on what you do best and let us do the rest.

Contact us if you’re curious about how Vendo helps maximize merchant profits. We’re happy to have a conversation about how we can support you and simplify the burdens of credit card processing.

About Vendo: Vendo offers comprehensive payment processing services to e-commerce merchants. Our innovative, AI-powered tools offer merchants simple, secure, and seamless payment solutions, along with expert customer support from integration to end-user concerns. Our expert team works 24/7 to shape your vision into reality.